Blue Cross Blue Shield of Oklahoma Open Enrollment

How much could you save on 2022 coverage?

Compare health insurance plans in Oklahoma and check your subsidy savings.

Image: guruXOX / stock.adobe.com

Oklahoma health insurance marketplace 2022 guide

Six insurers offer 2022 coverage in state's exchange

- Louise Norris

- Health insurance & health reform authority

- January 20, 2022

Oklahoma exchange overview

Oklahoma uses the federally facilitated exchange/marketplace, which means enrollees use HealthCare.gov. For 2022, there are eight insurers offering plans in the Oklahoma exchange. Marketplace rates increased by 5.9% on average for 2022.

Frequently asked questions about Oklahoma's ACA marketplace

Oklahoma uses the federally facilitated exchange/marketplace, which means enrollees use HealthCare.gov.

Oklahoma defers to the federal government to review rate filings for ACA-compliant products (most states conduct their own rate review, but Oklahoma, Texas, and Wyoming do not).

Then-Governor Mary Fallin's administration initially showed some openness to a state-run exchange — if only as a slightly less distasteful option than a federally operated exchange. The Oklahoma Joint Committee on Federal Health Care Law studied exchange options and issued its final recommendations in February 2012. The committee supported a state-run exchange open to small businesses, but not individuals. A bill for this type of exchange, which was similar to Utah's exchange, was introduced but not passed in 2012.

In line with state leaders' opposition to the ACA, Oklahoma is not actively marketing the exchange to residents. However, three state organizations received grants to act as navigators starting in 2013: Cardon Outreach in Oklahoma City, Oklahoma Community Health Centers, Inc., and Little Dixie Community Action Agency, Inc. By 2018, Little Dixie Community Action Agency, Inc. was still a navigator organization, although the other two agencies were no longer receiving navigator grants. In their place, the Latino Community Development Agency secured a navigator grant of $120,000 in 2018. In 2019, only Legal Aid of Oklahoma received a navigator grant, amounting to $300,000. Legal Aid of Oklahoma again received the only navigator grant in 2020, but it was larger, amounting to more than $373,000.

HHS is running the exchange in Oklahoma. You can compare plan, determine subsidy eligibility and enroll in coverage at Healthcare.gov.

For 2022, there are eight insurers offering plans in the Oklahoma exchange. This includes two newcomers: Friday Health Plans (in the Tulsa and Oklahoma City areas) and Centene/Celtic (branded as Ambetter in Oklahoma). The following insurers will offer coverage for 2022, with varying coverage areas:

- Bright Health

- BCBSOK

- Oscar

- Medica

- CommunityCare

- UnitedHealthcare

- Friday Health Plans

- Ambetter (Centene/Celtic)

Insurer participation in Oklahoma's exchange has been steadily growing over the last few years, from one insurer in 2017 and 2018 to eight in 2022. In addition to the two new insurers for 2022, Oklahoma gained three new exchange insurers as of 2021 (Oscar, UnitedHealthcare, and CommunityCare HMO; CommunityCare already offered coverage in Oklahoma outside the exchange; their plans became available in the exchange for 2021).

In addition to Oklahoma, South Carolina, Wyoming, Alaska, Delaware, Iowa, Mississippi, and Nebraska each had just a single insurer participating in the exchange for 2018. But Iowa, South Carolina, and Oklahoma each gained another exchange insurer in 2019. In 2020, Alaska, Mississippi, and Nebraska gained additional insurers, and for 2021, Wyoming gained a second insurer. Delaware is the only state that continues to have just one insurer offering plans in its marketplace as of 2021, and that's still the case for 2022.

Oklahoma had four carriers in its exchange in 2015, but only two in 2016, and just one in 2017 and 2018. But Medica joined the exchange statewide in 2019, and Bright Health has joined the exchange in Oklahoma City as of 2020.

UnitedHealthcare was new to the Oklahoma exchange for 2016, but offered plans outside the exchange in 2015. They exited the exchange at the end of 2016.

Blue Cross Blue Shield of Oklahoma no longer offered the Blue Choice provider network in the individual market as of 2016 (but continued to offer it in the group market). There were about 40,000 insureds in Oklahoma who had to switch to plans that use the Blue Advantage or Blue Preferred networks — both of which are PPOs, but narrower than Blue Choice. The Blue Advantage network is concentrated in the Tulsa and Oklahoma City metro areas, and is not available at all in 25 of the state's 77 counties. Most existing enrollees were eligible for auto-renewal, but Blue Choice network insureds who opted for auto-renewal were mapped to a plan with a different network. Blue Cross Blue Shield of Oklahoma ended up with 95 percent of the exchange market share for 2016.

CommunityCare stopped offering plans in the exchange at the end of 2015. They had fewer than 2,000 insureds as of late 2015.

Global Health offered plans in the exchange in 2015, but exited the individual market at the end of 2015.

Time/Assurant exited the individual market nationwide at the end of 2015.

Enrollees who had coverage through Global Health, CommunityCare, and Time/Assurant needed to select new coverage from one of the carriers offering plans in 2016. Although according to Lexology, those three carriers accounted for less than three percent of Oklahoma's exchange enrollees in 2015. The exchange had 108,614 effectuated enrollees as of June 2015, so there were somewhere around 3,200 people who are impacted by the withdrawal of those three carriers from the market in Oklahoma. The rest of the enrollees — about 97 percent of the total in 2015 — were covered under Blue Cross Blue Shield of Oklahoma plans.

Aetna participated in the exchange in Oklahoma in 2014, but exited the exchange (and the entire individual market in Oklahoma) just prior to the start of open enrollment for 2015 coverage. They did not offer individual market coverage in Oklahoma in 2015 or 2016, on or off-exchange.

But for 2017, they had indicated that they would rejoin the Oklahoma exchange, albeit only in the metropolitan areas of Tulsa and Oklahoma City. Aetna's exchange plans did appear in the Oklahoma SERFF filings for 2017, although the carrier indicated earlier in the summer that their plan to rejoin the exchange for 2017 had not yet been finalized.

In early August, Aetna announced that they were canceling their plans to expand their exchange presence in 2017. They already offered coverage in 15 exchanges, but had planned to expand into five more in 2017, including Oklahoma. Their change of heart meant that Blue Cross Blue Shield was the only carrier offering plans when open enrollment for 2017 got underway in November 2016.

That continued to be the case for 2018 as well, but Oklahoma's exchange got a new insurer in 2019 when Medica joined statewide. And Bright Health has joined the exchange in the Oklahoma City area as of 2020.

For 2021, Oscar, UnitedHealthcare, and CommunityCare HMO joined the exchange in Oklahoma, bringing the number of participating insurers to six. And for 2022, Friday Health Plans will join, with coverage available in the Tulsa and Oklahoma City areas.

The open enrollment period for 2022 coverage ran from November 1, 2021 to January 15, 2022. Outside of open enrollment, a qualifying event is necessary to enroll or make changes to your coverage. If you have questions about open enrollment, you can read more in our comprehensive guide to open enrollment.

For 2022 coverage, Oklahoma's exchange insurers are implementing the following average rate changes, which amount to an overall weighted average increase of about 5.9%:

- Bright Health: 4.27% increase.

- BCBSOK: 4.11% increase.

- Oscar: 1.8% decrease

- Medica: 8.2% increase

- CommunityCare: 0.8% increase

- UnitedHealthcare: 5.93% increase

- Friday Health Plans: New for 2022, so no applicable rate change

- Ambetter (Centene/Celtic): New for 2022, so no applicable rate change

But a weighted average rate change doesn't tell us much about how a particular enrollee's rates will change in the coming year:

- The published rates only apply to full-price plans, but most enrollees are eligible for premium subsidies and thus do not pay full price. For these enrollees, annual rate changes depend on how their own plan's rates are changing, as well as any changes in their premium subsidy amount (which depends on the cost of the benchmark plan, as well as the enrollee's projected income for the coming year).

- Overall average rate changes do not account for the annual rate increases that apply due to increasing age. A person who has individual market coverage for several years will continue to pay more each year — just due to the fact that they're getting older — even if their health plan has an overall rate change of 0% during that time.

- A weighted average, by definition, lumps all the plans together. But different insurers offer plans in each region, and each insurer's rate change is different. So the rate change that applies to a given enrollee can vary quite a bit from the average.

For perspective, here's a look at rate changes in Oklahoma's exchange in previous years:

- 2021: Rates virtually unchanged; three new insurers joined exchange. Oklahoma gained three new insurers in its exchange for 2021. For the existing insurers that offered plans in 2020, overall average premiums in 2021 were very similar to what they were in 2020. Blue Cross Blue Shield of Oklahoma had the bulk of the market share, and their overall rates for 2021 were essentially unchanged from 2020. Medica decreased premiums by more than 5%; Bright Health increased premiums by almost 2%.

- 2020: Slight average increase for existing plans; Bright joined exchange. The following average rate changes applied in Oklahoma's exchange for 2020 (enrollment is listed in terms of the number of policyholders; a policy can cover a single individual or multiple family members):

- Medica: 9.4 percent decrease. According to Medica's filing in SERFF, they had 3,383 policyholders in Oklahoma in 2019.

- BCBSOK: 3 percent increase. According to BCBSOK's filing In SERFF, they had 100,605 policyholders in Oklahoma in 2019.

- Bright Health: New to the state, so no rate change (plans available in Oklahoma City area)

- 2019: Average rate decrease of 2%; Medica joined exchange. For 2017 and 2018, Blue Cross Blue Shield of Oklahoma was the only insurer offering plans in the Oklahoma exchange. But Medica announced in June 2018 that they would join the Oklahoma exchange for 2019, with coverage available statewide. Blue Cross Blue Shield of Oklahoma implemented an average premium decrease of 2 percent for 2019. The Oklahoma Insurance Department noted that the average rate changes varied from a decrease of about 11 percent to an increase of about 8 percent.

- 2018: Average increase of about 8%. Blue Cross Blue Shield of Oklahoma proposed an overall average rate increase of 8.3%, which was far lower than the national average proposed rate increase for 2018. In August, the proposed average increase was revised to 7.8%, which was deemed justified by federal regulators. However, Oklahoma had proposed a reinsurance program that would have resulted in premiums for 2018 declining by an average of about 34% instead of increasing by 8.3%. The state's waiver proposal to obtain federal funding for the reinsurance program was ultimately withdrawn (details below), so pre-subsidy rates ended up increasing slightly in Oklahoma in 2018, rather than decreasing sharply.

- 2017: Average increase of 76 percent (by far the largest percentage increase in the nation). Blue Cross Blue Shield of OK initially filed average proposed premium increases for 2017 that ranged from 49.8 percent to 51.7 percent, with an overall average of 49.2 percent. But in August 2016, BCBSOK filed a new rate increase proposal, with an overall average rate increase of 76 percent across their entire block of ACA-compliant individual market business in Oklahoma (range was 58.2 percent to 96.7 percent). As explained below, the rates for 2017 included the cost of cost-sharing reductions added to the premiums, which didn't start to happen until 2018 in the rest of the country. BCBSOK noted that they had 163,992 people enrolled in ACA-compliant individual market plans as of August 2016, including both on and off-exchange members. CCIIO's rate review process does not give the federal government the power to deny rate increases, so it was unsurprising when state officials confirmed in October 2016 that the proposed rate increases would take effect in January without any modifications. But most enrollees were receiving premium subsidies, and the subsidies grew sharply to cover the higher premiums.

- 2016: Average increase of 26 percent. UnitedHealthcare was new to the exchange for 2016. For the plans that UnitedHealthcare offered outside the exchange in 2015, the average approved rate increase was 12.5 percent for 2016. BCBS of OK proposed a 31.2 percent average rate increase across all of their ACA-compliant plans. The rates that were ultimately approved ranged from 22 percent to 34 percent, with an average increase of 25.8 percent. The approved rate increase for Blue Preferred PPO plans ended up at 32 percent, which was significantly lower than the 44 percent rate hike the carrier had proposed. For Blue Cross Blue Shield's PPO multi-state plan and the Blue Advantage PPO, the approved rates were very similar to what was proposed.Statewide, the average benchmark premium (second-lowest-cost-Silver plan) in the Oklahoma exchange was 35.7 percent more expensive in 2016 than it was in 2015. This was the sharpest increase in any of the 37 states that used Healthcare.gov in 2015.

- 2015: Average increase of 12.2 percent. Across the four existing exchange carriers, premium changes for 2015 ranged from a decrease of 9.1 percent to an increase of 29 percent, averaging 12.2 percent. Two new carriers (GlobalHealth and CommunityCare) joined the exchange in 2015, adding to the options that enrollees had in some areas of the state.

During the open enrollment period for 2021 coverage, 171,551 people enrolled in private individual market plans through Oklahoma's exchange. This was a record high for the state, and was an 8% increase over 2020 enrollment.

Oklahoma's exchange enrollment reached record highs in 2019, 2020, and again in 2021. Nationwide, across all states that use HealthCare.gov, enrollment peaked in 2016 and trended downward each year until 2021, when it started to increase again. Despite having a federally-run exchange and leadership that's fairly opposed to the ACA, Oklahoma bucked the trend with enrollment increases in 2017, 2019, and 2020.

During the COVID-related enrollment window in 2021, more than 37,000 Oklahoma residents signed up for coverage through the marketplace. This was more than double the normal pace of enrollments at that time of year (when a qualifying event would normally be required to enroll; qualifying events were not necessary during the COVID-related enrollment period in 2021).

Enrollment in Oklahoma's exchange in prior years (during open enrollment) was as follows:

- 2014: 69,221 people enrolled

- 2015: 126,115 people enrolled

- 2016: 145,329 people enrolled

- 2017: 146,286 people enrolled

- 2018: 140,184 people enrolled

- 2019: 150,759 people enrolled

- 2020: 158,642 people enrolled

- 2021: 171,551 people enrolled

Would ACA subsidies lower your health insurance premiums?

Use our 2022 subsidy calculator to see if you're eligible for ACA premium subsidies – and your potential savings if you qualify.

Obamacare subsidy calculator *

Estimated annual subsidy

Provide information above to get an estimate.

* This tool provides ACA premium subsidy estimates based on your household income. healthinsurance.org does not collect or store any personal information from individuals using our subsidy calculator.

Oklahoma enacted legislation calling for another reinsurance waiver proposal, but waiver is not being pursued

In 2017, Oklahoma submitted 1332 waiver proposal to CMS, seeking federal pass-through funding for a reinsurance program (details below). But the waiver proposal wasn't submitted until August, and the state withdrew it in late September, when it was clear that CMS approval was not going to happen in time for 2018 premiums to be adjusted (rates were expected to decrease by about 34 percent if the reinsurance program had been implemented, but instead, rates increased by an average of just under 8 percent).

In the 2018 legislative session, lawmakers again considered a reinsurance program. S.B.1162 passed the Senate in March, passed the House in April, and was signed into law in early May. The legislation initially called for the state to seek federal pass-through funding in addition to state-based funding that would be generated by fees assessed on health insurers in the state, but the amended version of the legislation removed the ability for the state to assess fees, and instead called for the state to only seek federal funding for a reinsurance program. But the bill clarified that the Marketplace Stabilization Program (the reinsurance program) "may accept funding from other sources."

Federal "pass-through" funding for reinsurance is generated when a state's reinsurance program results in lower premiums, which, in turn, result in smaller premium subsidies. The amount that the federal government saves on premium subsidies is passed on to the state (assuming a 1332 waiver has been approved) and used to fund the reinsurance program. Several states have already implemented reinsurance programs using federal pass-through funding in addition to state-based funding, with health insurance premiums that are now lower than they would have been without the reinsurance programs.

But while Oklahoma enacted legislation to get the ball rolling on a reinsurance program, the state has not moved ahead with the 1332 waiver process. Trevor Brown, state capitol reporter for Oklahoma Watch, noted soon after the bill passed that Oklahoma did not have immediate plans to submit a 1332 waiver, and the legislation was passed as a backup measure, in case they want to submit a reinsurance proposal in the future. It's also noteworthy that the yes votes on S.B.1162 in the House came exclusively from Republicans. There were no House Democrats in favor of S.B.1162. The Oklahoma State Department of Health confirmed in June 2018 that no action had been taken, nor was any currently being planned, in terms of a 1332 waiver.

And for 2019, as noted above, Blue Cross Blue Shield of Oklahoma reduced their premiums in the individual market, and Medica joined the exchange statewide. The additional plan options and lower premiums may have made reinsurance less of a priority for Oklahoma, and the state has not moved to act on the reinsurance legislation in 2019.

BCBSOK had already added the cost of CSR to their rate increases for 2017, but they used broad load for 2017 and silver load for 2018

Throughout the summer and fall of 2018, insurers in most states were scrambling to add the cost of cost-sharing reductions (CSR) to their premiums for 2018. But in Oklahoma, they already did that — a year earlier. Blue Cross Blue Shield of Oklahoma was the only insurer offering plans in the exchange for 2018, and that was also the case for 2017. Their rate filing for 2018 noted that they added the cost of CSR to their premiums for 2018, but they did the same thing in 2016, when they filed rates for 2017.

So Blue Cross Blue Shield of Oklahoma essentially had the sort of rate hikes in 2017 that many insurers in other states implemented for 2018, with the cost of CSR newly added to premiums. That load was still incorporated into the 2018 premiums, but there wasn't much of a rate increase necessary, since it was already part of the 2017 rates, which were nearly adequate for 2018 as well.

But applicants in Oklahoma may have found that after-subsidy premiums were more affordable in 2018 than they were in 2017, due to the way the cost of CSR was handled. BCBSOK confirmed that although they added the cost of CSR to premiums in 2017 and again for 2018, they didn't use the same approach in both years. For 2017, the cost of CSR was added to the premiums for all of their plans (ie, "broad load"), whereas for 2018, the cost of CSR was added only to silver plans ("silver load" which is the approach that most states and insurers have taken since 2018).

Since premium subsidies are based on the cost of silver plans, subsidy amounts were much larger in 2018 in Oklahoma, despite the modest overall rate increase. And enrollees with premium subsidies found that after-subsidy prices for non-silver plans tended to be lower in 2018 than they were in 2017. Since the cost of CSR was added only to silver plan premiums in 2018 (and that continued to be the case for 2019), the rates for silver plans went up significantly more than the rates for other plans. The result has been larger premium subsidies, and particularly affordable coverage at other metal levels for people who are subsidy-eligible (people who can get CSR benefits should still consider a silver plan, since CSR benefits are only available on silver plans).

Amid HHS delays, state withdrew 1332 waiver reinsurance proposal in 2017

Oklahoma H.B.2406 was passed by the state legislature in May 2017, and signed into law by Governor Mary Fallin on June 6. The legislation called for the state to create a reinsurance program that would offset high-cost claims in the ACA-compliant individual market, both on and off-exchange. For each enrollee whose total claims exceed $15,000 during the year, the reinsurance program would have been designed to reimburse the insurer 80 percent of the total claims in excess of $15,000, up to a cap of $400,000 in claims (insurers would have been fully responsible for claims above that threshold, but those are rare).

Oklahoma planned to use federal "pass-through funding" in addition to assessments on insurers to fund the reinsurance program, with total funding of $325 million per year. In 2018, the state assessments on insurers were expected to generate $16 million (via a $0.76 per-member-per-month fee on health insurance plans sold in the state) and the other $309 million would come from the federal pass-through funding. But by 2022, the state assessment was expected to generate $56 million, with the per-member-per-month fee rising to $2.59 by that point.

The federal pass-through funding is the crux of the 1332 waiver. ACA Section 1332 allows states to use innovative programs (like reinsurance, in this case) to implement state-based reform. If the reform results in less federal spending on premium tax credits (premium subsidies), the state gets to use the savings to run their new program.

Oklahoma's 1332 waiver proposal for the reinsurance program was just the first step in their proposed reform plan, which would have involved additional 1332 waivers later on (details below). The first waiver proposal, submitted to HHS in August 2017, called for $309 million in pass-through funding for reinsurance in 2018, with gradually decreasing amounts for the following four years. The lower premiums that would result from the reinsurance program would, in turn, result in lower premium subsidies, since the subsidies wouldn't have to be as large to get the smaller premiums down to an affordable level. The state would then use the federal savings as pass-through funding to cover the bulk the cost of the reinsurance program.

The reinsurance program was also expected to result in more people with health insurance coverage, since premiums would become more affordable for those who don't qualify for premium subsidies and have to pay full price for their coverage. Oklahoma estimated that without the reinsurance program, they'd have 150,000 individual market enrollees (on and off-exchange), but with reinsurance, that number was projected to increase to 172,000. The waiver proposal noted that "without a reinsurance program, the Federal government will continue to pay high APTC amounts; with lower premiums, Oklahoma can make coverage accessible to more residents for the same amount of Federal dollars absent the waiver."

Oklahoma is one of just three states that does not have an effective rate review process and instead defers to the federal government for rate review of ACA-compliant health plans. In addition to granting federal pass-through funding for a reinsurance program, the 1332 waiver that Oklahoma submitted in August 2017 would also have transitioned the state to an effective rate review process as of plan year 2019.

Oklahoma submitted its 1332 waiver proposal in mid-August and requested a quick decision from HHS in order to implement the program for the 2018 plan year. After seeing an average rate increase of 76 percent (before subsidies) in 2017, rates were expected to decrease by about 34 percent for 2018 if the 1332 waiver had been approved in time to finalize those rates.

However, Oklahoma withdrew the waiver proposal on September 29, due to HHS delays in approving the waiver. The withdrawal letter states that HHS and Oklahoma had agreed that the approval would be complete by September 25, but that did not happen. September 27 was the deadline for insurer to commit to the exchange for 2018; the withdrawal letter states that "Oklahoma is forced to withdraw our waiver request due to failure of the Departments to provide timely waiver approval… While we appreciate the work of your [HHS and Treasury Dept.] staff, the lack of timely waiver approval will prevent thousands of Oklahomans from realizing the benefits of significantly lower insurance premiums in 2018."

The lack of timely response from HHS came despite the agency's March 2017 letter to states encouraging them to develop innovative approaches to health care reform via 1332 waivers. It's notable that Minnesota also submitted a 1332 waiver to establish a reinsurance program, but HHS approval was delayed by over a month, and came with an unexpected decrease in MinnesotaCare funding.

Oklahoma's ambitious plans for future innovation with a series of 1332 waivers

Thus far, Oklahoma has been one of the most hands-off states in terms of implementing the ACA. In general, they've rejected the ACA at every opportunity, and have deferred to the federal government on regulatory and enforcement measures.

Oklahoma did not establish its own exchange, did not expand Medicaid (although that will change by mid-2021, thanks to a ballot measure that voters approved in the summer of 2020), and filed an amicus brief in the King v. Burwell lawsuit, urging the Supreme Court to rule that ACA premium subsidies were illegal in states like Oklahoma that use HealthCare.gov (ultimately the Court ruled in 2015 that the subsidies were legal, preventing tens of thousands of Oklahoma residents from losing their subsidies).

But with all of that history, Oklahoma positioned itself in 2017 to propose a far-reaching innovation waiver under the ACA. Section 1332 of the ACA allows states to set up their own innovative approaches to health care reform, but there are rules involved: the state's proposal has to cover at least as many people, with coverage at least as comprehensive and affordable as it would be without the innovation waiver, and the state's approach can't create an additional financial burden on the federal government.

In March 2017, Oklahoma's Secretary of Health and Human Services published recommendations for a 1332 waiver. The state's goals were ambitious, and would involve Oklahoma taking a much more hands-on approach to health care reform. The state notes that "potential regulatory shifts at the federal level" (ie, the transition from the Trump Administration to the Obama Administration) provide the state the opportunity to make a variety of changes via the 1332 waiver system. Here's what the Oklahoma Department of Health and Human Services recommended, although the state has not moved forward with this (note that the only official 1332 waiver Oklahoma has submitted as of September 2017 is the one to obtain federal funding for the state's reinsurance program, which was withdrawn in September 2017 amid HHS delays in the approval process; the additional changes described below would require additional 1332 waivers that have not yet been submitted, and S.B.1162, passed in April 2018, only called for another 1332 waiver seeking federal funding for reinsurance, which the state has not pursued as of early 2019):

In 2018:

- The state would assume regulatory control over rates and plans, instead of deferring to the federal government for rate review (this would align with what nearly every other state already does). This provision was included in the 1332 waiver proposal that Oklahoma submitted in August 2017 and withdrew in September 2017.

- The state would also begin to focus on quality measures, value-based payments, and care coordination in an effort to decrease costs and improve quality.

- Oklahoma would allow a wider range of age-based premiums. The ACA caps the ratio at 3:1 for older versus younger enrollees. The AHCA, which was pulled before it reached a vote in the U.S. House, would have increased that ratio to 5:1. Oklahoma wants to implement something similar on a state level.

In 2019:

- Switch from HealthCare.gov to the Insure Oklahoma platform (Insure Oklahoma is a state-run program currently used for low-income residents; more details below)

- Establish "consumer health accounts" that would be similar to HSAs. The consumer health accounts would be funded with federal subsidy money, and the state is considering the possibility of automatic enrollment in individual market plans coupled with consumer health accounts (a similar proposal was part of the Patient Freedom Act, introduced earlier in 2017 by Senators Bill Cassidy (R, Louisiana) and Susan Collins (R, Maine).)

- The ACA's metal level designations would be eliminated, and replaced with two standardized benefit designs: either a robust, traditional plan, or a high-deductible plan that works with the consumer health accounts.

- The state would "re-evaluate and reduce" the ACA's essential health benefits requirements. The recommendations note, however, that preventive health care and behavioral health services (including substance abuse treatment) should be retained in the state's guidelines. Those services are of particular importance to the state's Native American tribes, and the 1332 waiver recommendations include efforts to preserve health care access and affordability for Native Americans (which was greatly expanded by the ACA).

- Subsidies (standardized based on age and income, so presumably not tied to the cost of insurance in a particular area) would be available to offset the cost of insurance for people with income in the 0-300 percent of federal poverty level range. Currently, ACA subsidies are available to those with income between 100-400 percent of federal poverty level. The 1332 recommendations note that nearly 40 percent of Oklahoma's uninsured population has income under the poverty level, and are thus not able to take advantage of the ACA's subsidies; the 1332 waiver would allow them access to affordable coverage (it's worth noting that the ACA called for covering those residents via Medicaid; the reason they're not eligible for assistance in Oklahoma is because the state has steadfastly refused to accept federal funding to expand Medicaid. In other words, it's an Oklahoma decision, rather than an ACA design flaw, that has left those residents uninsured; note that as of mid-2021, Medicaid will be expanded in Oklahoma under the terms of a ballot initiative that voters passed in 2020).

- The ACA's three-month grace period for overdue premiums (for people with premium subsidies) would be reduced to 30 days.

- Special enrollment period eligibility verification would be tighter (including the SEP that currently exists when an applicant is denied eligibility for Medicaid), and the state might consider changes to open enrollment structure, including tying enrollment periods to consumers' birthdays (as opposed to enrolling everyone at the same time during the year).

- Administrative processes for health insurers would be simplified, including requirements for reporting, risk mitigation, and enrollment.

Innovation waiver effective dates were allowed to begin in 2017. Thus far, several states have used 1332 waivers to create reinsurance programs, and Hawaii has a waiver that allows the state to forego the ACA's requirement that each state maintain a small business (SHOP) exchange.

State enacts legislation allowing out-of-state insurance sales

In May 2017, Oklahoma Governor Mary Fallin signed S.B.478 into law. The measure, dubbed the Health Care Choice Act, passed unanimously in the Senate, and 88-1 in the House. S.B.478 allows the state to enter into compacts with other states (approved by the legislature) so that health plans domiciled in those states could be sold to Oklahoma residents without having to obtain an Oklahoma certificate of authority (note that this is allowed under ACA Section 1333, although the Oklahoma Insurance Department noted that S.B.478 was "constructed and passed without regard to Section 1333 of the ACA").

But the insurer would have to obtain written permission from the Oklahoma Insurance Commissioner before offering coverage in Oklahoma. The approval process has not yet been developed, although the Oklahoma Insurance Department indicated that it will likely be more expedited than the process of obtaining a normal certificate of authority. Out-of-state insurers would be able to rent existing provider networks or create their own networks in Oklahoma, and HMOs would have to follow Oklahoma law in terms of HMO network adequacy requirements.

Changes to the bill made by a Senate committee require out-of-state plans to cover all benefits that are mandated in Oklahoma before the plan can be marketed in the state. Retaining this element of Oklahoma-based consumer protection was a key part of getting strong legislative support for the bill.

The Oklahoma legislation was intended to provide additional insurance alternatives in Oklahoma. The bill cannot, however, require insurers in other states to offer their plans for sale in Oklahoma, and it's unclear whether insurers in other states would be willing or able to establish provider networks and offer coverage in Oklahoma. According to the Oklahoma Insurance Department, out-of-state insurers had not yet expressed interest in offering plans in Oklahoma in the months following the enactment of S.B.478.

Rhode Island, Wyoming, Georgia, Kentucky, and Maine have all enacted laws over the last several years that allow out-of-state insurers to offer plans, but insurers have thus far not shown interest in doing so.

In 2018, as was the case in 2017, Blue Cross Blue Shield of Oklahoma was the only insurer offering individual market plans in the state. For 2019, Medica began offering coverage in Oklahoma, but they did so using the normal channels that an insurer uses when entering a new state, as opposed to participating in an out-of-state insurer compact.

H.B.1712, which was introduced in February 2017 but never advanced out of committee, would have allowed insurers to offer plans without various state-mandated benefits that predate the ACA (Oklahoma has 28 such mandates). It's important to note, however, that Oklahoma legislation cannot preempt the ACA, which is a federal law. That means health plans sold in Oklahoma — and every other state — still have to include the ACA's essential health benefits.

Oklahoma tried to eliminate premium subsidies for state residents

In June 2015, the Supreme Court issued a ruling in King v. Burwell, upholding subsidies in every state, regardless of whether the exchange is run by the state or federal government. Subsidies for 86,000 Oklahoma residents were safe.

Actuaries had predicted that the elimination of subsidies would have increased premiums by 55 percent (in addition to the regular annual rate increases based on medical cost growth) even for people who didn't receive subsidies. For those who were receiving subsidies, premiums would have increased by an average of 243 percent in Oklahoma. Because coverage would have become unaffordable for so many people, the size of the individual market would have dropped by about 70 percent, leaving only the sickest insureds with coverage.

But despite the disastrous outcome that would have resulted if the Supreme Court had eliminated subsidies in states like Oklahoma that use the federally-run exchange, Oklahoma was actively fighting to have the subsidies eliminated.

In late December, Oklahoma filed an amicus brief with the Supreme Court, urging the Court to side with King in the King v. Burwell hearing (ie, to do away with subsidies in states like Oklahoma that use Healthcare.gov). Five other states (Alabama, Georgia, Nebraska, South Carolina, and West Virginia) joined Oklahoma in filing the amicus brief. This is in contrast to Virginia, which headed a group of 18 states that filed an amicus brief in the similar Halbig v. Burwell case in November, but urging an opposite ruling, in favor of keeping the subsidies in all states regardless of who runs the exchange.

Oklahoma has also generated headlines because of a court ruling on the Oklahoma v. Burwell lawsuit over the legality of subsidies in states with a federally-run exchange. Oklahoma's Attorney General, Scott Pruitt, initiated the lawsuit. Last fall, a federal judge in Oklahoma ruled that subsidies cannot be issued by exchanges that are run by the federal government, but can only be issued in the 17 states where the state is running the exchange. That case was presented to the Supreme Court, but they declined to hear it, and the ruling in King v. Burwell (ie, that subsidies are legal in the federally-run exchange) overrides the lower court's decision in Oklahoma v. Burwell.

Following the Court's ruling on the King case, Oklahoma Governor Mary Fallon expressed her disappointment: "The Supreme Court's decision today in King v. Burwell means that taxpayers will be, for the time being, stuck with a law that is deeply flawed, disruptive to the lives of American families and a destructive force in our economy."

Oklahoma health insurance exchange links

Other types of health coverage in Oklahoma

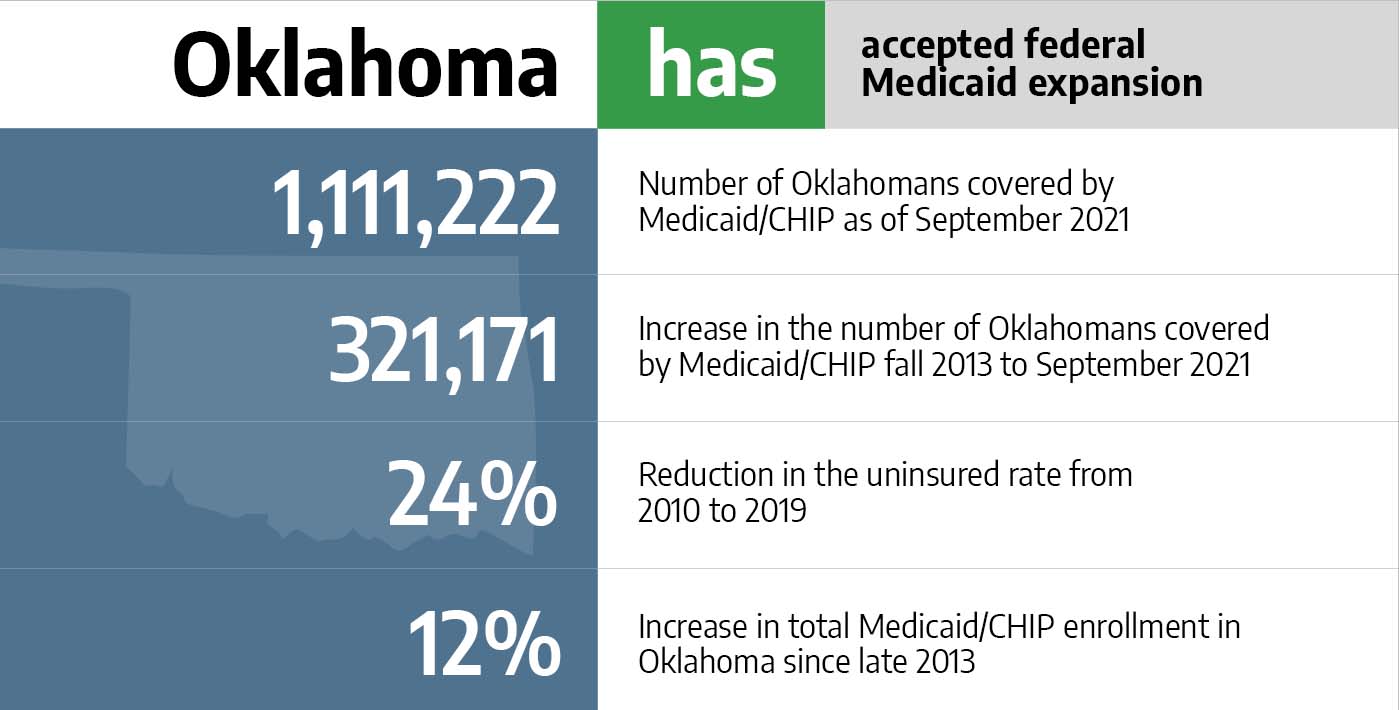

Medicaid in Oklahoma

Nearly 250,000 Oklahomans have enrolled since Medicaid expansion took effect July 1, 2021.

Medicare in Oklahoma

Oklahoma was among the first states to ensure access to Medigap plans for people under age 65.

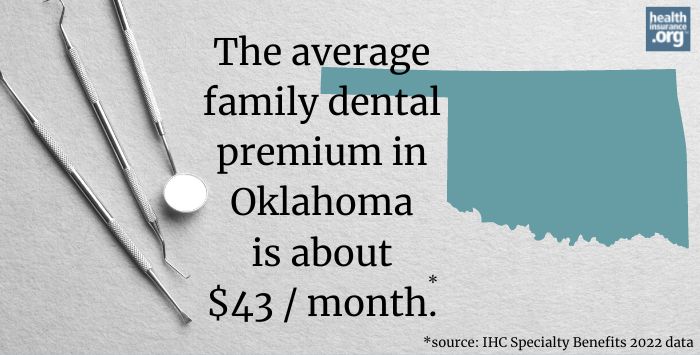

Dental Insurance in Oklahoma

Learn about adult and pediatric dental insurance options in Oklahoma, including stand-alone dental and coverage through the state's marketplace.

Source: https://www.healthinsurance.org/health-insurance-marketplaces/oklahoma/

0 Response to "Blue Cross Blue Shield of Oklahoma Open Enrollment"

Post a Comment